Define Correlation Matrix

Figure 1 - Add Correlation

Defining correlations (mutual relationships or connections) between input distributions in @RISK can be an important step in building a model. Input distributions are correlated when the values sampled for one (or more) distributions rely to some extent on the values returned by another distribution; they move, to some degree, in tandem - either in the same direction (positive correlation) or in opposite directions (negative correlation). When two or more input distributions are related, defining a correlation can help to ensure that a simulation does not return unrealistic results for the combination of distributions.

Adding a correlation to input distributions adds the RiskCorrmat property function to the @RISK distribution function. For example, the following input:

Correlations and copulas are two methods for modeling relationships between input distributions; adding or editing either a correlation or a copula in @RISK follows a very similar process. However, there are some key differences between the two elements, and in the potential outcomes for input distributions.

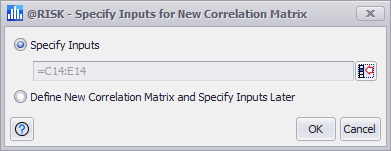

Specifying Inputs

Figure 2 - Specify Inputs Window

When creating a new correlation matrix, the first window that opens is the Specify Inputs window (Figure 2, right). The Specify Inputs window includes two options:

Once inputs have been specified, or if the option 'Define New Correlation Matrix and Specify Inputs Later' is chosen, the Define Correlation window will open. See Define Correlation Window for more information.